5 Last Minute Tax Filing Tips for Crypto Investors (+ Checklist)

Last-minute tax filing can be stressful, especially for crypto investors. Sorting through transactions, calculating gains, and following the IRS tax filing rules for digital assets can feel overwhelming.

If you’re struggling to meet the crypto tax deadline for 2025, you’re not alone. A 2024 Tax Procrastinators report found that 1 in 4 Americans feel unprepared to file their taxes, and 29% admit to procrastinating.

Filing crypto taxes at the last minute is tough, but it doesn’t have to be. This guide provides simple, actionable crypto tax tips to help you organize transactions, use helpful tools, and know when to seek expert advice. Let’s get started.

Important Update: Starting January 1, 2025, the IRS is changing how you track the cost basis for cryptocurrency. Instead of grouping all your wallets and exchanges together, you’ll need to track each one separately. Think of it like this: under the old rules, all your crypto was in one big bucket, so gains and losses were calculated by looking at the entire pool. Now, every wallet or exchange gets its own bucket.

For example, if you bought 1 Bitcoin on Coinbase for $20,000 and another on Kraken for $25,000, you could combine them to calculate an average cost basis of $22,500. But starting in 2025, if you sell Bitcoin from your Coinbase wallet, you can only use the cost basis of the Bitcoin in Coinbase—no mixing and matching with Kraken. This is similar to how stocks are tracked in separate brokerage accounts.

Read the full guide here.

Understanding Crypto Taxes: A Quick Refresher

In the U.S., cryptocurrencies aren’t treated as currency. The IRS classifies them as property. This means every time you sell, trade, or spend crypto, it’s a taxable event.

Here’s how it works:

- Selling crypto for cash is straightforward. The profit or loss is taxed as capital gains or losses.

- Trading one crypto for another (like Bitcoin for Ethereum) is taxable, even if you don’t touch fiat currency.

- Using crypto to pay for goods or services is the same as selling it. The IRS treats this as a sale.

- Earning through staking, mining, or airdrops counts as income. You’ll owe taxes based on the fair market value when you receive it.

Some actions aren’t taxable. For example, transferring crypto between wallets or simply holding it doesn’t trigger taxes.

When filing, report your gains and losses on Form 8949 and Schedule D. Gains are split into two categories:

- Short-term gains (held less than a year) are taxed at your income rate.

- Long-term gains (held over a year) are taxed at a lower rate—often 0%, 15%, or 20%.

If you earned staking or mining income, report it on Form 1040 as ordinary income.

Read our in-depth US crypto tax guide to learn more.

The IRS takes tracking crypto transactions seriously. They use advanced blockchain analytics tools like Chainalysis to follow the flow of crypto on public blockchains. These tools can link wallet addresses to real-world identities. Additionally, exchanges such as Coinbase and Kraken are required to report user data and transaction details under the Know Your Customer (KYC) rules. Starting in 2025, they’ll file Form 1099-DA to disclose even more transaction details.

If you fail to report accurately, the IRS can spot mismatches between what you report and what exchanges submit. This can lead to audits, fines, or even legal action. Interest on unpaid taxes also adds up quickly, increasing your liability.

The IRS uses one more strategy (arguably controversial) to track crypto transactions that we discuss here.

Understanding these basics ensures you file your crypto taxes without stress and focus on your investments.

5 Last-Minute Tax Filing Tips for Crypto Investors

1. Create an Inventory of all your Crypto Activities

Creating an inventory of your crypto activities is the first step to filing taxes quickly and accurately. But why is it so important?

While having all your data in one place does save time and reduce errors, the main goal—especially for last-minute crypto tax filing—is to understand what you’re dealing with. This helps you figure out whether you need extra tools or professional help to get everything done on time.

An inventory means organizing all your transactions, like buying, selling, trading, staking, mining, or engaging in DeFi activities such as yield farming and liquidity mining. Each of these has different tax rules, so clear categorization is crucial.

To get started, collect these key documents:

- Exchange reports, such as Form 1099 from Coinbase or Binance.

- Wallet transaction logs showing deposits, withdrawals, and transfers.

- Records of staking rewards, mining income, and airdrops, noting their fair market value (FMV) at the time you received them.

- Details of DeFi transactions, including yield farming or liquidity mining.

Read our guide on tracking crypto transactions to learn more about creating a detailed inventory.

If your transactions are simple and few, this process won’t take long. But for active traders or those with complex activities, using a tool like Bitcoin.Tax can make organizing faster and easier. If things still feel overwhelming, consulting a tax professional can be helpful.

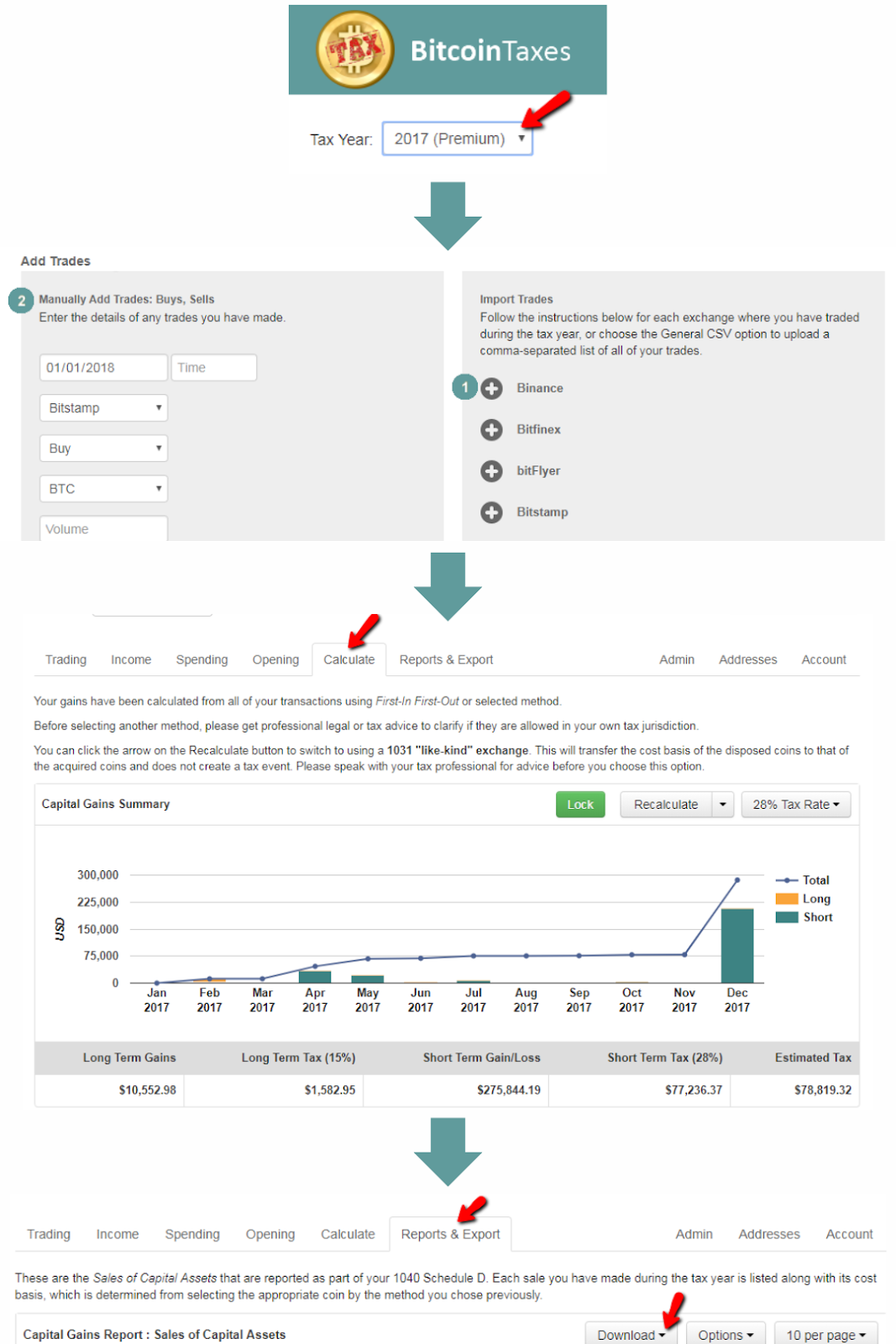

2. Use a Crypto Tax Software

Using crypto tax software is one of the best ways to simplify last-minute tax filing. It saves time, reduces errors, and ensures compliance. Platforms like Bitcoin.Tax streamline the process by consolidating your transaction history from multiple exchanges and wallets. They calculate your crypto gains and losses, track staking rewards, and even suggest tax-loss harvesting opportunities.

These tools automate complex calculations, like cost basis, and provide detailed reports formatted for IRS forms like Form 8949. This makes filing your crypto taxes faster and more accurate.

Here’s how to use Bitcoin.Tax:

- Export your transaction history as a CSV file from exchanges like Binance, Coinbase, or Kraken.

- Log into Bitcoin.Tax, go to “Import Trades,” select your exchange, and upload the file.

- For DeFi transactions, use Zerion.io to export your wallet history and upload it to Bitcoin.Tax.

- Review the data for accuracy, then download your tax report.

Check out our guide on importing crypto transactions to a tax tool for more details.

Bitcoin.Tax also integrates with TurboTax and TaxACT and is one of the best low-cost crypto tax filing tools out there.

Using a crypto tax software is one of the best crypto tax filing tips. It ensures your crypto taxes are accurate while saving you from unnecessary stress.

3. File a Tax Extension: Form 4868

Filing an extension lets you avoid rushing through your crypto tax filing process. This gives you an extra six months that you can use to properly claim crypto losses, deduct transaction fees, and stay compliant with IRS regulations while avoiding penalties for late filing. For crypto investors, this means more time to accurately report crypto gains, losses, and income.

Filing an extension is simple. Use IRS Form 4868, which you can submit online through the IRS’s Free File system or tax software like TurboTax. You can also download the form directly from here, fill it out, and mail it to the address for your location. Make sure it’s postmarked by the crypto tax deadline of 2025.

Remember, an extension only delays your filing, not your payment. You must pay your estimated taxes by the original deadline to avoid crypto tax penalties. If you’re unsure how to calculate taxes without filing, check out our step-by-step guide on filing a crypto tax extension and estimating payments.

Overall, filing an extension is one of the best last-minute tax filing tips for crypto investors to reduce stress and file accurately.

4. Pay your Crypto Taxes in Installments

Installments are a good option for last-minute tax filing, especially if your crypto taxes catch you off guard. Instead of risking fines, you can pay what you can upfront and set up a plan for the rest.

How?

These IRS payment plans break your tax liability into monthly payments, letting you stay compliant while avoiding penalties.

Here’s how it works:

- Short-Term Plans: For amounts under $100,000, you get 120 days to pay with minimal interest.

- Long-Term Plans: For up to $50,000, you can spread payments over 72 months by filing Form 9465.

- Partial Payment Plans: If you can’t pay the full amount, the IRS may approve reduced payments based on your finances.

Apply online through the IRS’s Payment Agreement tool, mail Form 9465, or call the IRS directly.

While installment plans ease the pressure, interest continues to accrue until you’re fully paid. So, we recommend using this option only if necessary, as installment plans come with extra costs that could make you pay more than your original tax bill. For more info, check out the official guide from the IRS.

5. Consult a Crypto Tax Professional

If your crypto taxes feel overwhelming, consulting a tax expert can save you time, stress, and potential penalties. Moreover, tax experts with crypto experience understand the unique challenges of IRS tax filing for digital assets. This is especially important for last-minute tax filing when there’s no room for mistakes.

Here are situations where it’s smart to get expert help:

High Transaction Volume: If you’ve made hundreds or thousands of trades across multiple exchanges, organizing your crypto gains and losses is challenging. While tools like Bitcoin.Tax can streamline the process, the risk of errors—like mismatched data, missing transactions, or incorrect cost basis—grows with transaction volume. In a last-minute rush, these errors might go unnoticed, leading to inaccurate filings and potential fines. A tax expert can catch and fix these issues quickly.

Complex Crypto Transactions: Activities like staking, yield farming, or liquidity mining often have unclear tax implications. For instance, liquidity mining rewards may trigger capital gains depending on how tokens are issued and burned. Tax professionals understand these nuances and ensure accurate reporting, avoiding IRS scrutiny.

Tax experts are also invaluable if you’ve missed reporting in previous years or received IRS notices. They can guide you through amending returns or setting up installment agreements. Additionally, they help you save more taxes by strategically claiming crypto losses, deducting transaction fees, and navigating new IRS cost basis rules.

Check out our in-depth guide on finding the right tax expert for your needs.

Final Checklist for Last Minute Crypto Tax Filing

When time is tight, having a clear plan can make last-minute tax filing less stressful. Use this checklist to stay on track and file accurately.

1. Gather Your Documents

- Wallet logs showing deposits, withdrawals, and transfers.

- Exchange forms like 1099s from Coinbase or Binance.

- Records of staking rewards, mining income, and airdrops with their fair market value at receipt.

- Proof of crypto-to-crypto trades and associated costs.

- Other documents like W-2s or 1099 from employment or freelance work paid in crypto and bank statements showing fiat conversions.

2. Double-Check for Mistakes

- Avoid math errors by using low-cost crypto tax filing tools like Bitcoin.Tax.

- Confirm all Social Security Numbers (SSNs).

- Ensure all forms are signed and dated.

- Report every transaction to avoid crypto tax penalties, even those without profits or tax implications (like crypto gifts over $18,000).

3. File or Request an Extension

- File electronically for faster processing. Bitcoin.Tax can generate IRS forms and integrate with TurboTax.

- If you’re not confident that you can meet the crypto tax deadline for 2025, submit Form 4868 to request an extension. Remember, extensions delay filing, not payment.

- You can also consult a tax expert if necessary.

4. Review Before Submitting

Remember, filing accurately helps you avoid IRS penalties and potential audits, but mistakes aren’t the end of the world. You can always amend your taxes later and avoid penalties if you act quickly. See our guide on how to amend crypto taxes to learn more.

FAQ

Will the IRS know if I don’t report my crypto?

Yes, the IRS can find out if you don’t report crypto. Exchanges report transactions to the IRS, and tools like Chainalysis track blockchain activity. If you fail to report, you risk penalties, interest, or audits. Always report all transactions to stay compliant.

Can I file crypto taxes late?

Yes, you can file your crypto taxes late, but you may face penalties and interest on unpaid taxes. Filing an extension with Form 4868 gives you more time to file, but the taxes you owe for your crypto gains and income must still be paid by the deadline.

What is the penalty for not paying crypto tax?

The penalty for not paying crypto tax includes 0.5% of the unpaid tax per month, up to 25%. Interest also accrues daily on the unpaid amount. Paying as much as possible by the deadline can reduce these costs. Check out our in-depth guide on crypto tax penalties to learn more.