DeFi Tax Reporting: Complete Guide

DeFi tax reporting is simple once you understand the basics.

But then, why is there so much confusion? Many countries haven’t released specific guidelines for DeFi transactions. Plus, some DeFi activities are more complex than others, dividing even the experts on their tax treatment.

The Jarrett’s staking rewards lawsuit is a great example of this confusion. You can read about it here.

In this guide, we’ll explain the underlying tax mechanics and how they apply to DeFi transactions. Additionally, we’ll cover the tax implications of common DeFi activities and practical tips for accurate tax reporting.

What is DeFi?

DeFi, short for Decentralized Finance, is a new financial system that works without traditional intermediaries like banks. Instead, it uses blockchain technology and smart contracts on platforms like Ethereum and Solana.

This allows people to conduct peer-to-peer transactions directly with each other. DeFi provides various financial services, including lending, borrowing, trading, and earning interest, all without needing a bank or other middlemen.

Common Taxable DeFi Transactions

In the context of taxes, DeFi activities can quickly get complex. However, once you understand the underlying reasoning and pattern, it’s actually quite simple.

The following are some of the most common DeFi transactions and their tax implications.

Staking and Yield Farming:

Staking means locking up some of your cryptocurrency in a blockchain network to help it run by validating transactions. In return, you earn rewards. These rewards are usually considered taxable income.

It’s similar to crypto mining, but for cryptocurrencies that use a proof-of-stake system, like Ethereum after the merge. In contrast, cryptocurrencies like Bitcoin use mining and a proof-of-work system.

Income Tax: Rewards from staking are considered income and are taxed at regular income tax rates.

Example: You stake 1 ETH and receive 0.05 ETH as a reward. If the market value of 0.05 ETH at the time of receipt is $100, you report $100 as income. Additionally, If you decide to sell the 0.05 ETH later, any increase in value since the time you received it will be subject to capital gains tax.

Trading Crypto:

Trading involves swapping one crypto for another or fiat currency on decentralized exchanges. Each trade is a taxable event. You need to calculate capital gains or losses based on the difference between the purchase and sale prices.

Capital Gains Tax: Profits from selling or exchanging cryptocurrencies are subject to capital gains tax. The tax rate depends on how long you hold the crypto and your local tax laws.

Example: You buy 1 BTC for $30,000 and later trade it for 10 ETH when BTC’s market value is $35,000. Your capital gain is $5,000 (selling price – purchase price).

Lending and Borrowing:

In DeFi, you can lend your crypto assets to earn interest or borrow against your crypto holdings. Interest earned from lending is usually taxable while borrowing itself isn’t typically a taxable event unless the collateral is sold or liquidated.

Interest Income Tax: Interest earned from lending crypto assets is treated as income and is taxable.

Capital Gains Tax: If you sell the collateral to repay a loan, this may result in a capital gain taxable event.

Example: You lend 1 BTC and earn 0.05 BTC as interest over a year. If the market value of 0.05 BTC at the time of receipt is $2,500, you report $2,500 as income.

Suppose you borrow 1 ETH using 2 ETH as collateral, and the collateral is liquidated for some reason. If the selling price is higher than what you initially paid for those 2 ETH, the difference may be subject to capital gains tax.

Airdrops and Forks:

Airdrops distribute free tokens to users, and forks create new cryptocurrencies from existing ones.

Income Tax: Free tokens received through airdrops or forks are typically considered taxable income, with the received tokens usually being treated as income based on their fair market value at the time of receipt. However, in some countries, receiving airdrops is tax-free. More on this later.

Airdrop Example: You receive 100 tokens from an airdrop, and their market value at the time of receipt is $300. You report $300 as income.

Fork Example: A blockchain you hold tokens in undergoes a fork, and you receive 50 new tokens worth $500. This $500 is considered taxable income.

DeFi Taxes in Different Countries

Tax authorities worldwide are paying more attention to crypto transactions, including DeFi activities. Here are the key points:

Income Tax: Rewards from staking, yield farming, liquidity mining, and airdrops are typically considered income and are taxable.

Capital Gains Tax: This applies when you sell, exchange, or trade cryptocurrencies. You need to calculate capital gains or losses based on the difference between the purchase price and the selling price.

Transaction Reporting: Most countries require centralized crypto exchanges to follow the Anti-Money Laundering Act. This means they must verify user identities and report transactions. So, if there’s a mismatch between what your exchange reports and what you report on your tax return, tax authorities will find out.

However, DeFi platforms often escape these requirements since they don’t always have a central authority.

Despite this, you still have to pay taxes. Tax evasion is a crime, whether you use a centralized exchange (CEX) or a decentralized exchange (DEX). Keep detailed records of all DeFi transactions to report income and capital gains accurately.

Here’s an overview of global tax regulations and specific rules in major jurisdictions.

United States:

The Internal Revenue Service (IRS) considers crypto as property. Taxable events include trading, spending, selling, and earning rewards from staking and yield farming (like lending interest and liquidity mining rewards).

Check out our in-depth US tax guide to learn more.

European Union:

The tax treatment of cryptocurrencies varies by country. Generally, income from staking, yield farming, and airdrops is taxable, and capital gains tax applies to trading activities.

In some countries, income earned from DeFi activities may even be tax-free. Check out our list of crypto-tax-free countries to learn more.

United Kingdom:

HMRC, like most other countries, treats crypto as property. Income from staking and yield farming is taxable, and capital gains tax applies to trading. Taxpayers must report income and capital gains on their self-assessment tax returns.

Check out our in-depth UK tax guide to learn more.

Canada:

The Canada Revenue Agency (CRA), unlike other countries, considers crypto as commodities. While the CRA hasn’t released specific guidelines on DeFi taxes, income from staking, yield farming, and airdrops is likely considered taxable income based on existing laws. Capital gains tax applies to trading.

Check out our in-depth Canada tax guide to learn more.

Australia:

The Australian Taxation Office (ATO) treats crypto as property. Income from staking and yield farming is taxable income, and capital gains tax applies to trading.

Check out our in-depth Australia tax guide to learn more.

We couldn’t cover all the countries in this guide as that would be a) not relevant and b) make this guide longer than necessary.

So, check out our country-specific crypto tax guides. Each guide is dedicated to the tax laws of a specific country.

How to Track and Report DeFi Transactions

Accurate tracking of transactions is essential for proper DeFi tax reporting. Here are some best practices for tracking your transactions:

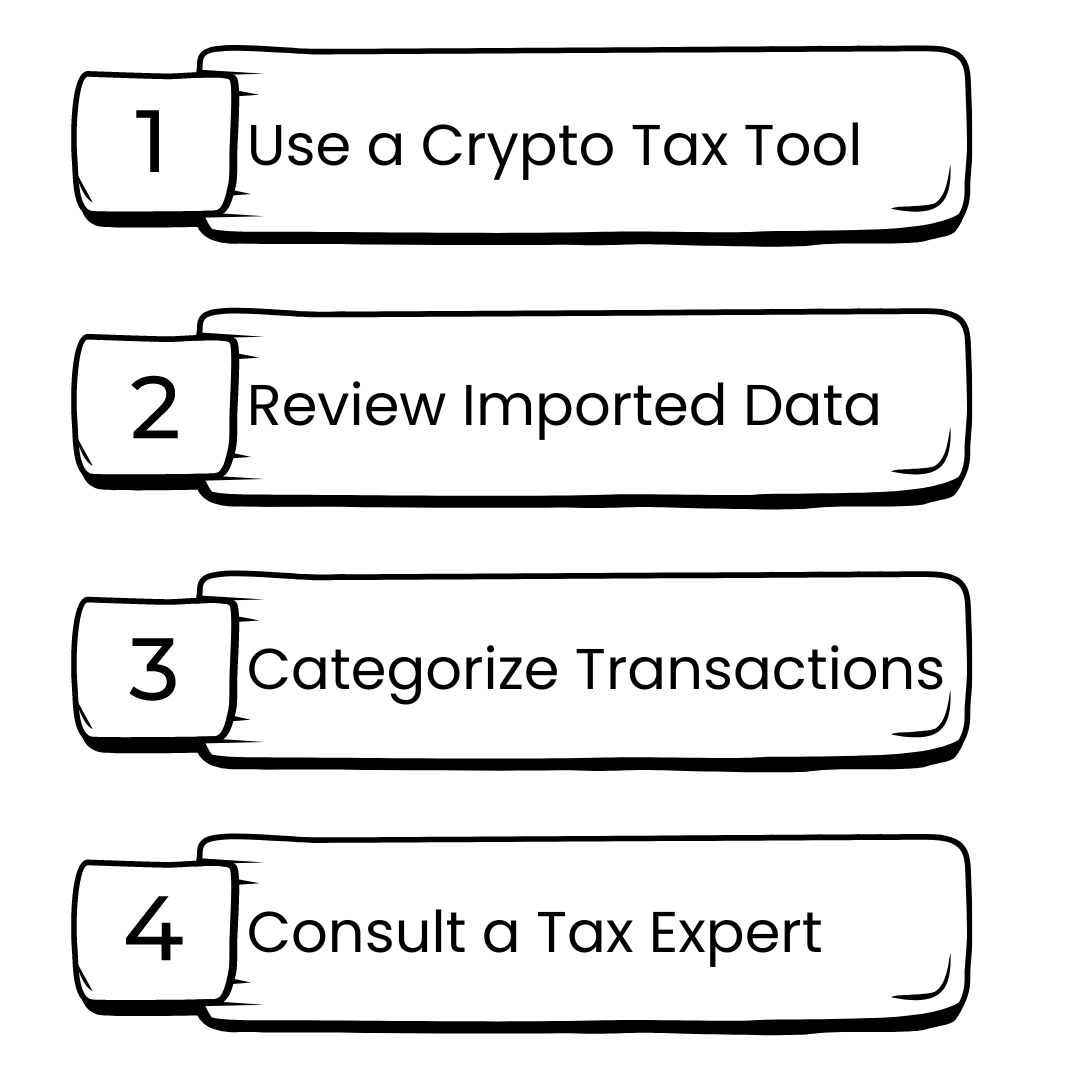

Use a Crypto Tax Tool: Bitcoin.Tax simplifies tax reporting by tracking transactions from multiple wallets and exchanges. It calculates your taxes based on your country and creates the relevant tax reports.

Review Imported Data: Check the imported data for accuracy. Manually add any missing transactions or correct any errors. This is actually one of the most common challenges with crypto tax tools. Additionally, regularly update your transaction records to avoid missing details. Sync your wallets and exchanges with tracking tools frequently.

Categorize Transactions: Sort transactions by type (e.g., staking rewards, trades, liquidity mining). This helps identify taxable events and calculate taxes accurately. Bitcoin.Tax can do this for you automatically.

Consult a Tax Professional: Consider consulting a tax professional if:

- You have many wallets and exchange accounts.

- You’re involved in complex DeFi activities.

- Large sums of money are involved.

- You’re being audited.

If you’re still unsure, read our complete guide on choosing a tax professional, which explains when to consult one and when not to.

FAQ

Are DeFi transactions taxable?

Not all DeFi transactions are taxable. However, common taxable events include:

- Receiving staking or yield farming rewards

- Trading cryptocurrencies

- Earning interest from lending

Borrowing and transferring assets between your own wallets are generally not taxable unless the collateral is sold or liquidated.

Does DeFi Platform report to the IRS?

DeFi platforms do not directly report to the IRS. Unlike centralized exchanges, DeFi platforms operate on decentralized platforms without a central authority, so they don’t automatically send transaction data to tax authorities.

However, you still need to report your DeFi transactions and earnings to the IRS. Using crypto tax tools can help you track and report your DeFi activities properly. If you’re unsure about your obligations, consult a tax professional.

Does DeFi use KYC?

Most DeFi platforms do not use KYC (Know Your Customer) procedures. Unlike centralized exchanges, DeFi platforms are decentralized and usually don’t have a central authority to enforce KYC rules. This means users can often trade, lend, and borrow without providing personal information.

However, some DeFi platforms may use KYC to comply with regulations or for extra security. Always check the platform’s policies to understand their KYC requirements.

What records do I need to keep for DeFi transactions?

You should keep detailed records of all DeFi transactions, including:

- Date and time of the transaction.

- Type of transaction (e.g., trade, stake, lend).

- Amount and value of the crypto involved.

- Platform or wallet used.

- Any associated fees.

- Fair market value at the time of receipt.

Can transaction fees be deducted from my taxable income?

Transaction fees can often be deducted from your capital gains. For example, if you paid a fee to execute a trade, you can include this fee in the cost basis of the transaction. This reduces your taxable gain. Read this to learn how to reduce your crypto taxes.