Tax Reporting for Crypto Day Traders: The Best Solution

Tax reporting for crypto day traders can be very challenging because day traders make many small, frequent trades throughout the day. This can quickly add up, making it hard to keep track of everything. Many of the options available to help with this problem are either not effective enough or too expensive.

So, what’s the solution?

That’s what we’ll find out today. But first, let’s quickly cover the basics.

Understanding Crypto Day Trading

Crypto day trading is when people buy and sell cryptocurrencies within the same day to make quick profits from small price changes. Unlike long-term trading, which involves holding onto assets for a long time, day trading means making many quick trades.

Common trading pairs include BTC/USD, ETH/BTC, and XRP/ETH. Traders use strategies like scalping, which aims for small profits from tiny price changes, and range trading, which involves buying and selling within a set price range. Some of this, if not most, is often automated using crypto bots you can build yourself.

Crypto day traders often rely heavily on technical analysis and indicators like Moving Averages (MA), Relative Strength Index (RSI), and Bollinger Bands.

Check our guide on crypto charts and indicators to learn more.

But why do day traders struggle with tax reporting? Since day traders aim to make small but multiple frequent profits throughout the day, the transactions can quickly add up. For example, a typical day trader might make 50 to 100 trades daily, adding up to 1,500 to 3,000 trades each month. In contrast, a swing trader might make only 10-20 trades monthly.

Check out our in-depth guide on the best crypto trading strategies.

Tax Implications of Crypto Day Trading

Crypto day trading comes with a lot of tax implications because you’re buying and selling so often. Every single trade is a taxable event, so you have to report your gains or losses each time.

For example, if you buy Bitcoin for $30,000 and sell it for $32,000, that $2,000 profit gets taxed. On the flip side, if you lose money, you can deduct that loss. With so many trades, figuring out your cost basis and gains can get really complicated.

That’s why keeping good records is super important to stay on the right side of tax laws and avoid any hefty penalties.

Common Tax Reporting Challenges for Crypto Day Traders

Now that we’ve touched on the challenges of tax reporting for crypto day traders, let’s get specific and discuss the most common ones you might face.

Volume of Transactions: If you’re day trading, and especially high-frequency trading, you could be making thousands of trades daily. Imagine trying to track all those by hand – it’s just not practical.

Data Import and Missing Trades: You probably use multiple exchanges and wallets, right? Each has its own data format, and sometimes information gets lost in translation. This can make importing data a real headache.

Accurate Calculations: Figuring out your capital gains and losses isn’t straightforward. You need to decide whether to use FIFO (first in, first out), LIFO (last in, first out), or specific identification methods. Each method affects your taxes differently, so getting it right is crucial. Check out our complete guide on accounting methods to learn more.

Regulatory Compliance: Tax laws are complex and include rules about adjusted cost basis, superficial losses, and 30-day rules. Missing any of these can lead to trouble with the tax authorities. It’s a lot to keep track of, especially if you’re doing it manually.

Time-Consuming Process: Manually calculating and generating reports for a high volume of transactions can eat up a lot of your time. It’s almost impossible to do it all by hand. There are tools that can help but… Well that’s the next point.

Software Limitations: Not all tax software can handle the volume of transactions that hardcore day traders deal with. Even if they can, the cost might be too high. Take TokenTax, for example. It’s popular, but its most expensive subscription at $1599 only supports up to 20,000 transactions – a drop in the bucket for serious traders.

The Solution

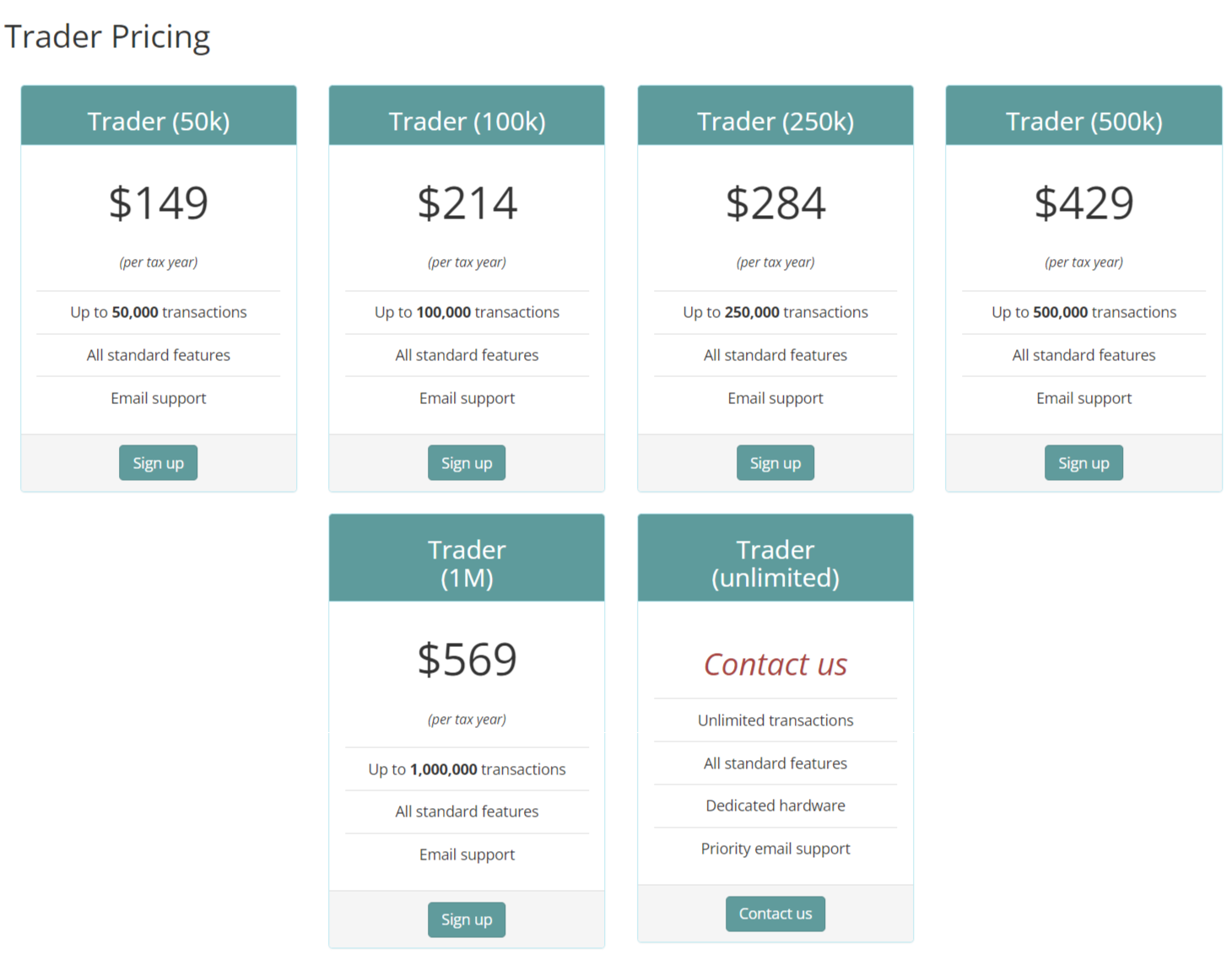

When it comes to tackling the tax reporting challenges of crypto day trading, Bitcoin.Tax is your best bet. This tool is designed to handle anywhere from 50,000 to 1,000,000 transactions, and and even more if needed.

You can easily import data from multiple platforms, and it provides precise calculations using methods like FIFO and LIFO. You can even switch your accounting method every tax year, which you can’t do if you report taxes manually.

Compared to other software, Bitcoin.Tax is both comprehensive and cost-effective. For instance, Bitcoin.Tax’s lowest tier at $149 supports up to 50,000 transactions, whereas TokenTax’s most expensive tier at $1599 only supports up to 20,000 transactions. Despite its affordability, the service remains top-notch, as shown by our loyal user base.

Check out our tight community on Reddit for tax tips and more.

Other Features

One standout feature is its API integration with major exchanges and wallets, so you can import trading histories directly from your accounts. If you prefer, you can export your data as a CSV file and then import it into Bitcoin.Tax.

Bitcoin.Tax supports almost all major exchanges, including Binance, Coinbase, Gemini, Exodus, Kraken, Bitstamp, KuCoin, and Crypto.com. We are always updating our exchange compatibility based on user feedback. Bitcoin.Tax also calculates capital gains for NFTs and DeFi trading.

The primary report you’ll use is the capital gains report, which can be exported in various formats, including ones friendly for tax software and accountants. They also offer income reports for miners, donation reports for gifts and tips, margin reports for margin trading (Kraken only), and a closing report that shows year-end holdings and unrealized gains—crucial for tax planning. All of this is based on where you live and your local tax laws.

In summary, Bitcoin.Tax is affordable, efficient, and reliable—everything you need in the best crypto tax software.

FAQ

What is crypto day trading, and how does it affect my taxes?

Crypto day trading involves buying and selling cryptocurrencies within a single day to profit from short-term price movements. Each trade is a taxable event, meaning you must report gains or losses for every transaction.

Why is tax reporting for crypto day trading so challenging?

The high volume of transactions, data import issues, accurate calculations, and regulatory compliance make tax reporting complex and time-consuming for crypto day traders.

How does Bitcoin.Tax help with tax reporting for day traders?

Bitcoin.Tax simplifies the process by supporting a high volume of transactions, allowing seamless data import from multiple platforms, and providing accurate calculations based on various accounting methods.

Can Bitcoin.Tax handle transactions from multiple exchanges and wallets?

Yes, Bitcoin.Tax supports nearly all major exchanges and wallets, including Binance, Coinbase, Gemini, Exodus, Kraken, Bitstamp, KuCoin, and Crypto.com.

How does Bitcoin.Tax compare to other crypto tax software?

Bitcoin.Tax is more cost-effective and comprehensive than other software. For example, its lowest tier at $149 supports up to 50,000 transactions, while TokenTax’s most expensive tier at $1599 only supports up to 20,000 transactions.